Navigating Payout Velocity Patterns Across Regional Mobile Banking Integrations for Slot Play

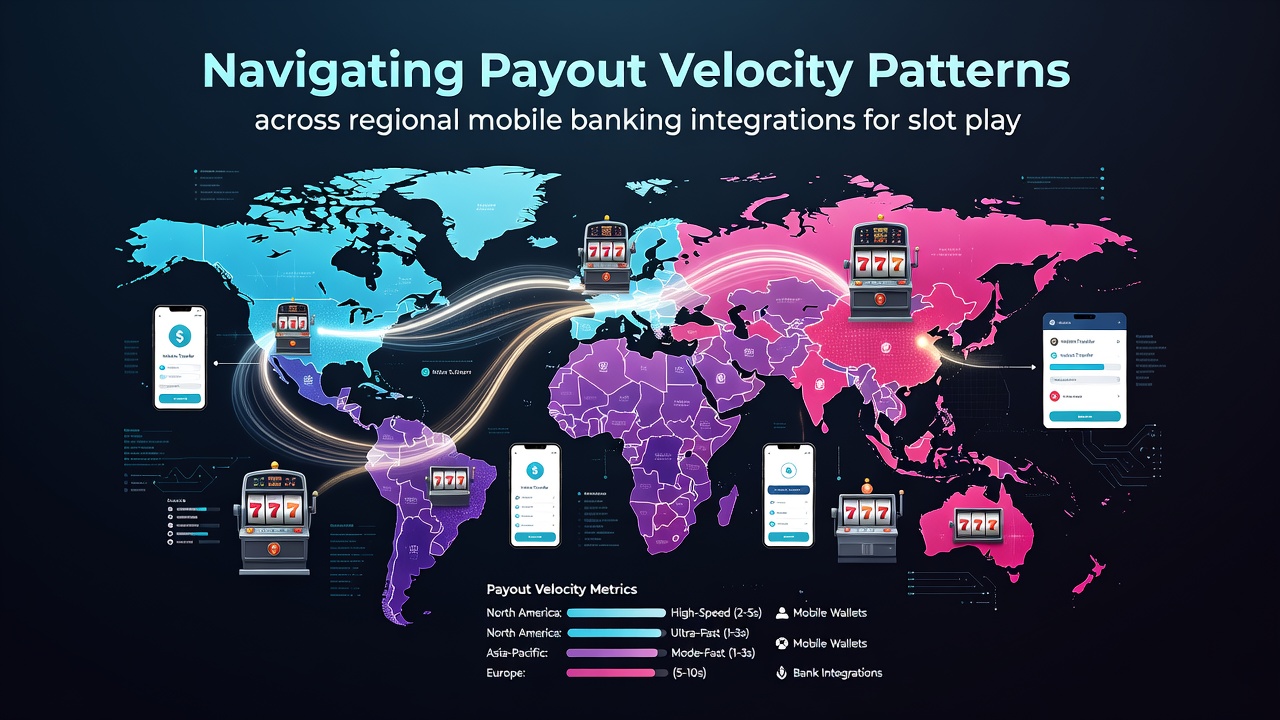

Observers note that payout velocity in mobile slot environments depends heavily on how banking integrations align with local payment rails, and patterns emerge when comparing processing times across North America, Europe, and Asia-Pacific markets. Data from payment system reports shows that ACH transfers in the United States typically clear within one to three business days while instant payment options tied to same-day settlement networks reduce that window to minutes in supported states. Those who've examined transaction logs find that verification layers, including identity checks required by state regulators, often add hours even when the underlying rail supports faster movement.

Observers note that payout velocity in mobile slot environments depends heavily on how banking integrations align with local payment rails, and patterns emerge when comparing processing times across North America, Europe, and Asia-Pacific markets. Data from payment system reports shows that ACH transfers in the United States typically clear within one to three business days while instant payment options tied to same-day settlement networks reduce that window to minutes in supported states. Those who've examined transaction logs find that verification layers, including identity checks required by state regulators, often add hours even when the underlying rail supports faster movement.North American Integration Patterns

Regional banking partners in the United States and Canada handle slot winnings through distinct channels that produce measurable velocity differences. Federal Reserve data indicates that real-time payment systems such as the FedNow service, expanded in recent years, now connect dozens of mobile banking applications used by slot platforms operating in states with legal iGaming. Yet adoption rates vary because some institutions still route requests through legacy overnight batch processes, creating a split where certain users receive funds the same day while others wait until the next business cycle.

Canadian systems present a contrasting picture because Interac e-Transfer protocols allow near-instant domestic transfers once initial account linking completes. Industry reports from the Canadian Gaming Association reveal that operators integrating these rails see average payout completion times drop below thirty minutes in provinces where regulations permit direct wallet-to-bank movement. Observers tracking July 2026 transaction volumes noted a further uptick in same-day processing after several large banks completed API upgrades that reduced manual review steps for verified accounts.

European and Asia-Pacific Rail Comparisons

SEPA Instant Credit Transfers dominate European mobile banking setups connected to slot operators, delivering funds in under ten seconds when both sending and receiving institutions participate in the scheme. Research published by teh European Payments Council shows participation rates above 80 percent among major banks in the eurozone, although cross-border transfers involving non-euro currencies introduce additional settlement delays of up to one hour. In parallel markets such as Australia, the New Payments Platform enables similar real-time movement, and figures from the Australian Payments Network indicate that slot-related withdrawals processed through NPP rails now account for more than half of all digital payouts recorded in the first half of 2026.

What's interesting is how these regional rails interact with operator-side compliance engines. Automated fraud detection algorithms flag a percentage of transactions for manual review regardless of rail speed, and studies from academic payment research centers find that the added step extends overall velocity by an average of 45 minutes in high-volume jurisdictions. Operators that pre-verify user banking details during initial registration reduce the frequency of such flags, producing more consistent payout windows across different geographic footprints.

Factors Influencing Velocity Consistency

Multiple technical and regulatory elements shape whether a given mobile banking integration delivers predictable payout speeds. Network latency between the gaming platform and the bank’s API endpoint can introduce variability measured in seconds to minutes, while peak traffic periods around major sporting events or promotional campaigns sometimes queue requests even on instant rails. Data aggregated by regional banking associations shows that weekends and public holidays extend processing times in markets that lack 24/7 settlement, creating weekly patterns visible in transaction analytics dashboards.

Security protocols also play a documented role. Multi-factor authentication steps required by certain banks add friction that slows the final transfer stage, although biometric methods increasingly replace older SMS-based codes and shorten that interval. One study of transaction metadata across multiple operators found that accounts using biometric confirmation completed payouts 28 percent faster on average than those relying on traditional verification sequences.

Operational Adjustments by Operators

Platform providers respond to these velocity patterns by maintaining relationships with multiple banking partners in each region, routing requests dynamically based on current rail performance. When one integration experiences temporary slowdowns, traffic shifts to an alternate provider that maintains faster baseline speeds for the same jurisdiction. Reports compiled by payment consultancy groups indicate that such routing logic now appears in the majority of large-scale mobile slot deployments, resulting in more stable average completion times reported to users.

Regulatory timelines further influence strategy. Jurisdictions that mandate daily reconciliation reports sometimes require operators to hold funds until verification completes, overriding technical capabilities of the banking rail. Those who monitor compliance calendars adjust payout scheduling accordingly, aligning release windows with both regulatory deadlines and the fastest available settlement options.

Conclusion

Patterns in payout velocity across regional mobile banking integrations for slot play reflect the combined effects of local payment infrastructure, verification requirements, and operator routing decisions. Figures from multiple payment networks demonstrate that instant rails shorten timelines significantly when fully adopted, yet residual compliance steps and network variability continue to produce measurable differences between regions. Continued expansion of real-time settlement systems, alongside incremental improvements in API connectivity, points toward narrower velocity ranges in coming periods as more institutions complete integration upgrades.